Chapter 8.B – Functional Form 1: Linearity (continued)

8.5 Marginal effects and elasticities

In the preceding sections of this chapter, it was shown that OLS estimation techniques can be applied to the estimation of a variety of functional forms. Once these equations have been estimated, however, it is often useful to measure the magnitude of the effect resulting from a change in an independent variable. For example, when a market researcher estimates a demand equation, it is important to know the magnitude of the change in quantity demanded that results from a change in price or income. To measure the magnitude of effects such as this, economists generally rely on two alternative measures:

- marginal effects, and

- elasticities.

The marginal effect associated with a change in an independent variable is, roughly speaking, the change in the dependent variable that occurs when there is a one-unit change in the level of an independent variable. Suppose, for example, that a dependent variable ([latex]Y[/latex]) is a function of [latex]k[/latex] independent variables [latex](X_{1},X_{2},\ldots ,X_{k})[/latex]. The marginal effect associated with a change in [latex]X_{j}[/latex] can be measured as:[1]

[latex]\text{marginal effect of }X_{j}\text{ on }Y\text{ = }\frac{\Delta Y}{\Delta X_{j}}[/latex]

holding constant the level of all other independent variables.

| Model | Equation | Marginal Effect | Elasticity |

|---|---|---|---|

| Reciprocal | [latex]Y_i=\beta_0+\beta_1\frac{1}{X_i}[/latex] | [latex]-\beta_1/X^2[/latex] | [latex]-\beta_1/XY[/latex] |

| Log-Log | [latex]ln(Y)=ln(\beta_0)+\beta_1ln(X)[/latex] | [latex]\beta_1Y/X[/latex] | [latex]\beta_1[/latex] |

| Linear log | [latex]Y=\beta_0+\beta_1ln(X)[/latex] | [latex]\beta_1/X[/latex] | [latex]\beta_1/Y[/latex] |

| Log-linear | [latex]ln(Y)=\beta_0+\beta_1X[/latex] | [latex]\beta_1Y[/latex] | [latex]\beta_1X[/latex] |

| Linear | [latex]Y=\beta_0+\beta_1X[/latex] | [latex]\beta_1[/latex] | [latex]\beta_1X/Y[/latex] |

| Quadratic | [latex]Y=\beta_o+\beta_1X+\beta_2X^2[/latex] | [latex]\beta_1+2\beta_2X[/latex] | [latex]\frac{(\beta_1+2\beta_2X)X)}{Y}[/latex] |

| Cubic | [latex]Y=\beta_0+\beta_1X+\beta_2X^2+\beta_3X^3[/latex] | [latex]\beta_1+2\beta_2X+3\beta_3X^2[/latex] | [latex]\frac{(\beta_1+2\beta_2X+3\beta_3X^2)X)}{Y}[/latex] |

In many cases, however, economists wish to measure the magnitude of an effect using a measure of elasticity. As noted in section 8.4.1, the elasticity of [latex]Y[/latex]with respect to[latex]X_{j}[/latex] is a measure of the percentage change in [latex]Y[/latex] that results from a one-percent change in the level of [latex]X_{j}[/latex]. In mathematical terms, this elasticity can be expressed as:

elasticity of [latex]Y[/latex] with respect to [latex]X_{j}[/latex] =[latex]\frac{\%\Delta \text{ in }Y}{\%\Delta \text{ in }X_{j}}[/latex]

When estimating demand functions, for example, economists are often interested in estimating the price elasticity of demand, the cross-price elasticity of demand, and the income elasticity of demand.

The Price Elasticity of Demand for Marijuana

Nisbet and Vakil (1972) attempted to measure the price elasticity of demand for marijuana among UCLA students. Using data from an anonymous survey (conducted by mail), they estimated both linear and double-log demand specifications. Using actual purchase data, the estimated equations were:

\begin{equation*}\widehat{\text{Qm}_i }= 3.236 – 0.225\text{Pm}_i – 0.002 \text{E}_i +0.036 \text{S}_i\end{equation*}

\begin{equation*}\widehat{ln(\text{Qm})} = 2.609 – 01.013 ln(\text{Pm}_i) – 0.311 ln(\text{E}_i) +0.404 ln(\text{S}_i)\end{equation*}

where:

- Qm[latex]_i[/latex] = quantity of marijuana purchased per month (in ounces)

- Pm[latex]_i[/latex] = price of marijuana (in dollars)

- E[latex]_i[/latex] = a measure of mean monthly expenditure

- S[latex]_i[/latex] = a measure of expenditure dispersion

In this sample, the average price of marijuana was $10 per ounce and the average quantity purchased was 1.49 ounces per month. As Table 8.1 indicates, under the linear specification, the price elasticity of demand (evaluated at the sample mean price and quantity) equals:

[latex]\hat{\beta}_{1}\left( \frac{\overline{Pm}}{\overline{Qm}} \right) = -0.225 \left( \frac{10.0}{1.49} \right) = -1.51[/latex]

Under the double-log specification, the estimated price elasticity of demand is simply equal to 1.013, the estimated coefficient on the log of the price variable.

As noted in Chapter 6, when a model is linear in variables the slope coefficients, [latex]\beta _{j}[/latex], serve as a measure of the marginal effect associated with a one-unit change in [latex]X_{j}[/latex], holding constant all of the other independent variables. Under the reciprocal, log, and polynomial models considered above, however, the marginal effect associated with a change in the level of an independent variable cannot be as simply measured. As noted above, the estimated intercept and slope parameters are measures of elasticities under the double-log specification. Under alternative model specifications, however, elasticities vary with the level of the dependent and/or independent variables. Table 8.1 provides a listing of the marginal effects and elasticities associated with a change in an independent variable under alternative model specifications.

An examination of Table 8.1 indicates that the marginal effect or elasticity associated with a particular independent variable may be a function of the level of either the dependent or the independent variable. When this occurs, economists often report the value of the marginal effects (or elasticities) measured at particular values of the dependent and independent variables.

In cross-sectional or longitudinal studies, the marginal effects (or elasticities) are generally reported for a “representative” observation. This generally means that the marginal effects are evaluated by setting the values of the independent variable(s) and the dependent variable to their sample means. In time-series analyses, however, economists are generally more interested in recent outcomes. Thus, marginal effects may be evaluated by setting the values of the dependent and independent variables equal to the most recently observed values.

A superficial examination of Table 8.1 may suggest that the use of the linear regression model is most appropriate when an economist is interested in estimating marginal effects, while the log-log specification should be used to estimate elasticities. Unfortunately, however, the simplest approach is not always the most appropriate approach. The choice among alternative functional forms should be based on the nature of the relationship that exists between the dependent variable and the set of independent variables. If it is believed that the marginal effect is constant for all levels of an independent variable, then a linear specification is most appropriate. If, however, it is believed that the magnitude of the marginal effect varies with the level of the independent variable, then an alternative functional form should be used that more closely approximates the economic process that generates the data.

8.6 Selecting a functional form

It should be noted that a regression model will often include more than one of the transformations described above. For example, it is quite possible that a regression model may be specified as:

[latex]Y_{i}=\beta _{o}+\beta _{1}\frac{1}{X_{i}}+\beta _{2}\ln (Z_{i})+\beta_{3}S_{i}+\beta _{4}S_{i}^{2}+u_{i}[/latex]

or:

[latex]\ln (Y_{i})=\beta_{0}+\beta_{1}X_{i}+\beta_{2}X_{i}^{2}+\beta_{3}Z_{i}+u_{i}[/latex]

In selecting the specific form of a regression relationship, an econometrician should take into account the nature of the relationship that exists between the dependent and independent variables. For example, the unemployment rate can never be less than 0% nor greater than 100%. If the unemployment rate is specified as either a dependent or independent variable, this characteristic should be taken into account (as in the reciprocal relationship discussed above). The earnings equation discussed below provides another case where economic theory provides some evidence that can be used to help select a model specification.

One strategy that is often used by practicing econometricians is to examine the model specifications used in previous studies of the same (or a closely related) topic. If previous researchers make a compelling case for a particular specification, then that specification often provides a useful starting point for future research. Of course, one should never accept an inappropriate model specification solely because it has been used before.

Quite often, however, the appropriate specification of an econometric model cannot be determined a priori. Prior studies may either not exist or may provide a variety of alternative model specifications. Under these circumstances, the choice of model specification is generally based upon empirical criteria.[2] An examination of appropriate empirical methods of selecting among alternative model specifications is the focus of Chapter 10.

For now, it can be noted economists sometimes select among alternative models by comparing the R[latex]^{2}[/latex] (or [latex]\overline{\mathrm{R}}^2[/latex]).of these models. While this approach is commonly used, a few qualifications should be made:

- Economists prefer to use economic theory to determine model specification. Those variables that are included in economic models because they are of theoretical importance should not be dropped from equations simply because this leads to a higher value of R[latex]^{2}[/latex] (or [latex]\overline{\mathrm{R}}^2[/latex]). R[latex]^{2}[/latex] is a measure of statistical association, and is not a measure of causation. Models based on causal relationships are expected to generate better predictions than models based on correlations that may be spurious.

- Since R[latex]^{2}[/latex] (or [latex]\overline{\mathrm{R}}^2[/latex]) provides a measure of the proportion of the variation in the dependent variable that is accounted for by the regression equation, it may be used to compare alternative models in which the dependent variable is the same. It is always inappropriate to use R[latex]^{2}[/latex] (or [latex]\overline{\mathrm{R}}^2[/latex]) as a criteria to select among competing models when the dependent variable differs across these models. For example, R[latex]^{2}[/latex] does not provide a meaningful comparison between linear and double-log models.

8.6.1 Example: An estimated earnings equation

The estimation of earnings equations has kept hundreds of econometricians busy for much of the past 25 years. By estimating variations of equation 8.29}, econometricians have been able to investigate such issues as: the rate of return to education, male-female wage differentials, racial wage differentials, and a wide variety of other issues. Let’s examine a simple earnings equation.

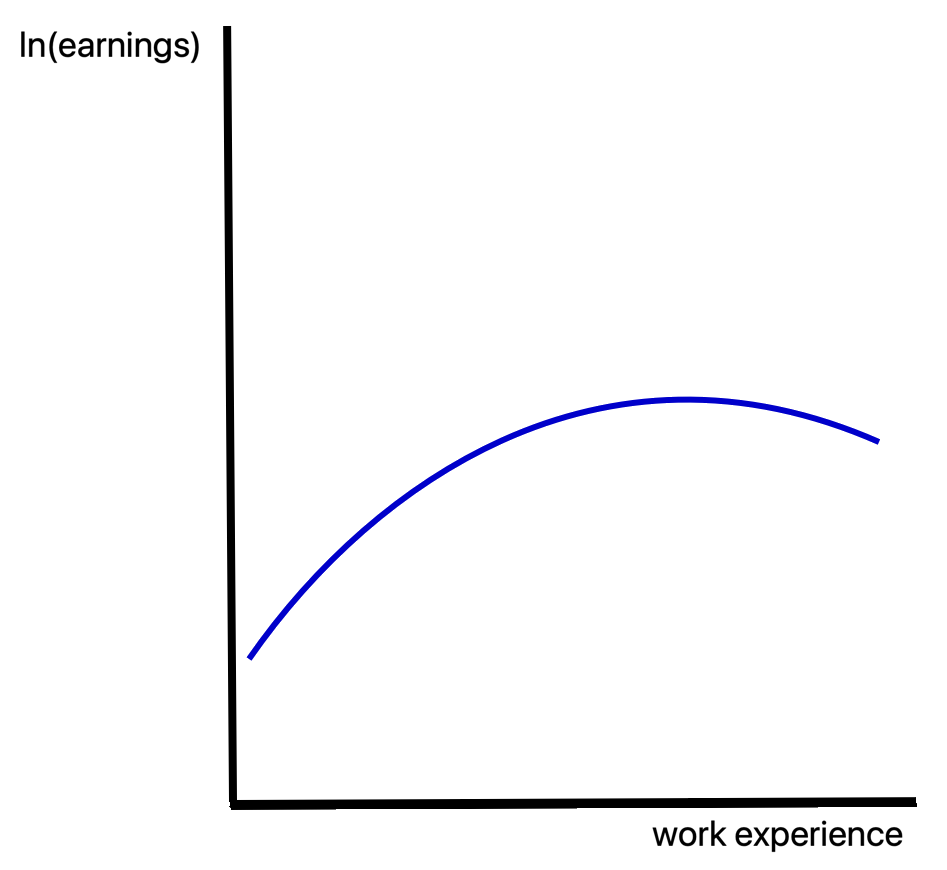

A large amount of theoretical work and empirical evidence indicates that earnings increase with work experience.[3] Earnings increase, however, by progressively smaller increments with each additional year of experience. Human capital theory provides a relatively simple explanation for this phenomena. The return to investments in education, health care, and on-the-job training are larger when the investment occurs at a relatively young age (since the benefits are realized over a longer time period). Thus, human capital investments tend to decline with age. Since human capital depreciates over time (as training becomes obsolete and skills deteriorate), earnings increase more rapidly during early stages of an individual’s career. As the individual ages, earnings will either increase more slowly, or may even decrease. Figure 8.8 illustrates the relationship between log earnings and work experience.

The discussion above suggests that an appropriate specification for an earnings equation is:

[latex]\ln(\mathrm{earnings}_i)=\beta_{0}+\beta_{1}\mathrm{experience}_i+\beta_{2}\mathrm{experience}^{2}+u_i \tag{8.31}[/latex]

where:

- earnings[latex]_{i}[/latex] = respondent’s earnings in 1985 (in 1985 dollars)

- experience[latex]_{i}[/latex] = months of work experience at the respondent’s two most recent jobs

This specification involves a combination of the log-linear and polynomial transformations. When the parameters of equation 8.31 are estimated using a sample of 3992 males that were participants in the National Longitudinal Study of the High School Class of 1972,[4]the estimated equation is:

\begin{equation}\widehat{\ln (\text{earnings}_{i})}=\underset{(236.95)}{9.377}+\underset{(10.676)}{0.01734}\text{experience}_{i}-\underset{(-5.780)}{0.0000904}\text{experience}_{i}^{2} \tag{8.32}\end{equation}

([latex]t[/latex]-ratios in parentheses)

Each of the estimated coefficients in equation 8.32 are significantly different than zero at all conventional significance levels. Notice that the estimated coefficient [latex]\hat{\beta}_{2}[/latex] is relatively small compared to the value of [latex]\hat{\beta}_{1}[/latex].[5] This combination of a positive value for [latex]\hat{\beta}_{1}[/latex] and a negative value (that is smaller in magnitude) for [latex]\hat{\beta}_{2}[/latex] is consistent with the inverted U-shaped earnings profile appearing in Figure 8.8.[6]

Since equations of this sort are often used to investigate the rate of return to education, let’s examine how the results appearing in equation 8.32 may be used for this purpose. Under this relatively standard specification, the percentage increase in earnings resulting from an additional year of education is given by:[7]

[latex]\%\Delta[/latex] in earnings[latex]_{i}[/latex] = ([latex](\beta _{1}+2\beta_{2})[/latex]experience[latex]_{i}\times 100\%[/latex]

Using the estimates appearing in equation 8.33, each additional month of work experience increases earnings by:

[latex]\%\Delta[/latex] in earnings[latex]_{i}[/latex]= [latex](0.01734-0.0001808) \times[/latex] experience[latex]_{i}) \times 100\% \tag{8.33}[/latex]

This equation suggests that the first month of work experience will, on average, cause earnings to increase by:

[latex](0.01734-0.0001808(1)) \times 100\% = 1.72\%[/latex]

An inspection of equation 8.33, however, indicates, that the percentage increase in earnings becomes progressively smaller as the level of work experience increases. For example, the 30th month of work experience will result in an average increase in earnings by:

[latex](0.01734-0.0001808(30)) \times 100\%=1.19\%[/latex]

In fact, this equation suggests that earnings will begin to decline for individuals who have received more than 96 months of work experience. This equation suggests that the 97th month of work experience results in a 0.02% decline in earnings. Is this result likely?

The simple answer to this is: “probably not.” The earnings equation estimated above is unlikely to provide very reliable information about the effect of additional work experience on earnings. It is likely that the earnings equation specified in equation 8.31 does not contain all of the variables that affect an individual’s earnings. In particular, individuals with higher levels of educational attainment tend to earn more. Since all of the individuals in this sample are approximately the same age, those with more education also tend to have less work experience. The relatively high rate of return to work experience for those with less work experience is likely to be partly due to the higher educational attainment of these individuals.[8] As will be shown more formally in Chapter 10, the omission of variables that belong in a regression model can result in biased estimates of model parameters.

In practice, most empirical studies do find that earnings decline beyond some level of work experience. In general, however, these studies tend to suggest that the decline in earnings occurs at a much higher level of work experience than is found using the relatively simple model discussed above. Thus, the specific estimates discussed above should not be taken too seriously. The method used to estimate the percentage increase in earnings resulting from an additional unit of work experience, however, can be applied whenever the dependent variable is the log of earnings and the independent variables include both an “experience” and an “experience[latex]^{2}[/latex]” term. While earnings equations tend to include a variety of additional right-hand side variables, virtually all of them use this basic specification.

In Chapter 9, we will examine a more elaborate earnings equation that takes work experience, education, and other variables into account.

8.7 Summary

In this chapter, it has been shown that the linear regression model can be applied to a wide variety of models after a suitable transformation of variables. The most commonly used transformations are the polynomial, reciprocal, and log transformations. These transformations substantially expand the range of models that can be estimated through linear regression techniques.

By carefully analyzing the process that generates the observed data, it is often possible to specify a functional form that provides a close approximation to the underlying relationship. When economic theory and knowledge of institutional processes does not provide such guidance, other criteria must be adopted to select an appropriate functional form. In simple bivariate relationships, plotting the data will often provide some guidance. Under the more general case of multiple regression analysis, however, a variety of empirical tests exist that may be used to guide specification choices. Tests of this sort will be discussed in Chapter 10.

The marginal effects and elasticities resulting from a change in an independent variable have also been addressed in this chapter. It was noted that, under most model specifications, the marginal effects and elasticities are functions of the level of the dependent variable, the independent variable, or both. The marginal effect is constant for all values of the dependent and independent variables only in the linear model. Elasticities are constant for all values of the dependent and independent variables only in the double-log model.

8.8 Key Concepts

- linearity

- linear in parameters

- linear in variables

- reciprocal transformation

- log transformation

- double-log models

- semi-log models

- linear-log models

- log-linear models]

- polynomial transformations

- marginal effects

- elasticity

8.9 Exercises and problems

- Which of the following models can be transformed into a model that is linear in variables? If such a transformation is possible, specify the transformation(s) and rewrite the model so that it is linear in the transformed variables.

- [latex]Y=\beta _{o}X_{1}^{\beta _{1}}X_{2}^{\beta _{2}}[/latex]

- [latex]Y=\beta _oX_1^{\beta _1\beta _2}X_2^{\beta _3}[/latex]

- [latex]Y=\beta _o+\beta _1\frac 1X+\beta _2X+\beta _3X^2[/latex]

- [latex]e^Y=\beta _oX^{\beta _1}[/latex]

- [latex]Y=e^{\beta _o+\beta _1X_1+\beta _2X_2}[/latex]

- Provide a graph of the function: [latex]Y=\beta_0+\beta_1\frac 1 X[/latex] assuming that:

- [latex]\beta_0 \lt 0[/latex] and [latex]\beta_1\gt 0[/latex]

- [latex]\beta_0 \lt 0[/latex] and [latex]\beta_1 \lt 0[/latex]

- What does the sign of [latex]\beta_1[/latex] imply about the nature of the relationship between [latex]Y[/latex] and [latex]X[/latex]?

- Consider the model given by:\begin{equation}Y_i=\beta_0+\beta _1\frac 1{X_i}+u_i \tag{8.34}\end{equation}

- Suppose that an econometrician uses this function to investigate the relationship between on-the-job injuries ([latex]Y_{i}[/latex]) and the level of government spending on OSHA and related programs ([latex]X_{i}[/latex]). What sign is expected for [latex]\beta_{0}[/latex] and [latex]\beta_{1}[/latex]? Draw a graph of this relationship. What is the interpretation of the value of [latex]\beta_{0}[/latex] in this model? Would this model be more or less appropriate than a linear model? Explain.

- Suppose that an econometrician buys a farm on which 100 acres of land have been planted with wheat. At harvest time, the econometrician divides up this land into 20 identical plots (5 acres / plot) and sends out 20 crews (varying the amount of labor on each crew, but providing the same amount of capital) to harvest the wheat on each plot. Each crew is given one day to harvest as much wheat as they can. The econometrician then gathers data and estimates a short-run production function using equation 8.34. What are the expected signs of [latex]\beta_{0}[/latex] and [latex]\beta_{1}[/latex]? Provide a graph of this relationship. What is the interpretation of [latex]\beta_{o}[/latex] in this case?

- Use the Phillips curve data in the file “phillips.dat” to estimate the following two Phillips curve models:\begin{equation*}\text{Inflation rate}_{t}\text{ = }\beta_{0}+\beta _{1}\left( \frac{1}{\text{Unemployment rate}_{t}}\right) +u_{t}\end{equation*}

\begin{equation*} \text{Inflation rate}_{t}\text{ = }\beta_{0}+\beta _{1}\text{Unemployment rate}_{t}+u_{t} \end{equation*}

(The results from the first equation should be the same as those appearing in equation 8.15.)

-

- What is the R[latex]^{2}[/latex] for each model?

- Is it reasonable to use R[latex]^{2}[/latex] to compare these two alternative models?

- Would it be as reasonable to use R[latex]^{2}[/latex] to compare alternative models that have different dependent variables (e.g., [latex]Y_{i}[/latex] and [latex]\ln (Y_{i})[/latex])?

- Consider the function: [latex]Y=\beta_{0}e^{\beta _{1}X}[/latex]

- Provide a graph of this function assuming that [latex]\beta_{0}[/latex] is positive and [latex]\beta_{1}[/latex] is negative.

- Transform this model into a linear model using an appropriate transformation of variables.

- Provide a graph of the relationship between the transformed variables.

- Use the data in the data file “phillips.dat” to:

- verify the estimates of the Phillips curve model presented in equation 8.15. Use your regression software package (or a spreadsheet) to plot the residuals from this regression equation vs. the independent variable.

- Estimate a linear version of the Phillips curve using the specification:\begin{equation*}\text{Inflation rate}_t\text{ = }\beta_0+\beta _1\text{Unemployment rate}_t+u_t\end{equation*}

- Use your regression software package to plot the residuals from this regression equation vs. the independent variable.

- Compare the [latex]R^2[/latex] of these two models. Which provides a better fit? Is there a pattern to the residuals in either of the two residual plots? If so, what does this suggest?

- One of the Phillips curve equations estimated by Lipsey (1960) was:

[latex]\text{rate of change in wage}_{t}=\beta_0+\beta_{1}\frac{1}{\text{UN}_{t}}+\beta_{2}\frac{1}{\text{UN}_{t}^{2}}+u_{t}[/latex]

where [latex]UN_{t}[/latex] = unemployment rate in year [latex]t[/latex]. In each of the models estimated by Lipsey, the estimated coefficients [latex]\beta_{1}[/latex] and [latex]\beta_{2}[/latex] were positive. What does this imply about the relationship between the rate of change in money wages and the unemployment rate?

- An econometrician estimates the following demand curve for good [latex]X[/latex]:\begin{equation*}\widehat{\ln (\text{Q}_{d})}=20.23-1.34\ln (\text{P}_{X})+0.35\ln (\text{P}_{Y})+0.67\ln (\text{Income})\end{equation*}

- What is the estimated price elasticity of demand for this good? Is demand elastic or inelastic?

- What is the estimated cross-price elasticity of demand between goods [latex]X[/latex] and [latex]Y[/latex]? Does it appear that goods [latex]X[/latex] and [latex]Y[/latex] are substitutes or complements?

- Is good [latex]X[/latex] a normal good or an inferior good? Is good [latex]X[/latex] a luxury or necessity? How can you tell?

- The file “service.dat” contains data on the amounts of capital and labor used to produce services in the U.S. economy during the period from 1948 to 1976.

- Use this information to estimate the parameters of a Cobb-Douglas production function.

- Test to determine whether a null hypothesis of constant returns to scale can be rejected at a 5% significance level.

- Use the data in the data file “deaths.dat” to estimate the instantaneous rate of growth for:

- the number of deaths.

- the U.S. population.

- the number of secondary school teachers.

- Suppose that a variable [latex]Y_{t}[/latex] grows according to the following formula:\begin{equation*}Y_{t}=\beta_{0}(1+g)^{t}e^{u_{t}}\end{equation*}

where:

- [latex]Y_{t}[/latex] = value of [latex]Y[/latex] at time [latex]t[/latex]

- [latex]\beta_{0}[/latex] = value of [latex]Y[/latex] at [latex]t=0[/latex]

- [latex]g =[/latex] rate of growth of [latex]Y_{t}[/latex]

- [latex]t =[/latex] time period}

- [latex]e[/latex] = base of natural logarithm

- [latex]u_{t} =[/latex]random error term

-

- Convert this model into a linear specification.

- Explain how the value of [latex]g[/latex] can be estimated. This growth rate is a measure of the compound rate of growth in the federal deficit.

- Use the federal budget deficit data in the file “deficit.dat” to estimate the parameters of this model for the tears 1970-1992.

- Suppose, instead, that the following model specification is used:\begin{equation*}Y_{t}=\beta _{o}e^{rt}e^{u_{t}}\end{equation*} where [latex]r[/latex] is the instantaneous rate of growth in the government deficit. Convert this model into a linear form and estimate [latex]r[/latex]. Can the regression results from part (c) be used here?

- Is the estimated compound rate of growth ([latex]g[/latex]) for deficit spending larger or smaller in magnitude than the estimated instantaneous rate of growth ([latex]r[/latex])? Will this always be expected to occur? Why or why not?

- Suppose that an econometrician had used one of these models to predict future deficits. Would these predictions have been very accurate? (Hint: Compare the outcomes for years after 1993 with the behavior of the deficit in prior years.)

- Suppose that an econometrician wishes to estimate an equation that captures the growth path in the government deficit over time.

- Is a log-linear model appropriate for this purpose (using data from the entire period)? Explain.

- Use a statistical software package (or spreadsheet package) to plot the government deficit during the entire period. Does this graph appear to be linear? Would a quadratic or cubic function provide a better fit?

- Estimate the parameters of the following two models:\begin{equation*}\text{Deficit}_{t}=\beta _{o}+\beta_{1}\text{Year}_{t}+u_{t}\end{equation*} and \begin{equation*}\text{Deficit}_{t}=\gamma _{o}+\gamma _{1}\text{Year}_{t}+\gamma _{2}\text{Year}_{t}^{2}+v_{t}\end{equation*} Which of these models provides a better fit? How can you tell?

- In this chapter, it was noted that the Cobb-Douglas production function exhibits constant exhibits constant returns to scale if the sum of the slope coefficients equals one. Increasing (decreasing) returns occur when the sum of these slope coefficients is greater (less) than one. Can estimates of the Cobb-Douglas production function be used to disprove the possibility of a U-shaped long run average cost curve? Explain.

- Walzer (1972) attempts to determine whether economies of scale are present in the provision of municipal police services in Illinois. As part of his study, he estimates the following average cost curve equation using a sample consisting of 31 cities in 1958;\begin{equation}\widehat{\text{AC}}_{i}=\beta _{o}-\underset{(3.94)}{0.00008}\text{Scale}_{i}+\underset{(1.69)}{0.0000000024}\text{Scale}_{i}^{2}+\underset{(5.81)}{0.00052}\text{PD}_{i} \label{8.35}\end{equation}\begin{equation*}+\underset{(5.40)}{3398.16}\text{PC}_{i}+\underset{(0.52)}{\text{0.386}}\text{CR}_{i}+\underset{(1.88)}{0.00038}\text{W}_{i}+\underset{(5.65)}{0.296}\text{Area}_{i}\end{equation*}\begin{equation*}\text{(}t\text{-ratios in parentheses)}\end{equation*}

where:

- [latex]AC_{i} = \frac{\text{municipal police expenditures}}{\text{quantity of service index for city }i}[/latex]

- Scale[latex]_{i} =[/latex] an index of the quantity of police services in city [latex]i[/latex]

- PD[latex]_{i} =[/latex]population density in city [latex]i[/latex]

- PC[latex]_{i}[/latex] = police officers per capita in city [latex]i[/latex]

- CR[latex]_{i}[/latex] = clearance rate = [latex]\frac{\text{offenses cleared by arrest}}{\text{offenses reported in city }i}[/latex]

- W[latex]_{i} =[/latex] average wage paid to recruits in city [latex]i[/latex]

- Area[latex]_{i} =[/latex]land area in city [latex]i[/latex]

-

- Explain why each of the variables are included in this equation.

- What do these estimates suggest about the presence of economies of scale?

- Gujarati (1968) estimates the following relationship:\begin{equation}\ln (\text{HWI}_{t})=\beta_{0}+\beta _{1}\ln(\text{UN}_{t}) \tag{8.36}\end{equation} using 24 quarterly observations on the help-wanted index (HWI[latex]_{t}[/latex]) and the unemployment rate UN[latex]_{t}[/latex]).

- What is the interpretation of the coefficient [latex]\beta_{1}[/latex] in this model? Can the sign of [latex]\beta_{1}[/latex] be predicted? Is a one-tailed or two-tailed test hypothesis test appropriate for estimates of [latex]\beta _{1}[/latex]

- Use the monthly data in the file “hwi.dat” to estimate the parameters of equation 8.36.

- At a 5% significance level, perform the hypothesis test selected in (a).

- Consider the money demand equation given by:\begin{equation}\ln (\text{M2}_{t})\text{ = }\beta_{0}+\beta_{2}\ln (\text{GDP}_{t})+\beta_{3}\ln (\text{Interest}_{t})+u_{t} \tag{8.37}\end{equation}

where:

- M2[latex]_{t} =[/latex]M2 measure of the money supply in year [latex]t[/latex]

- GDP[latex]_{t} =[/latex]real GDP in year [latex]t[/latex]

- Interest[latex]_{t}[/latex] = discount rate in year t

-

- What do the parameters [latex]\beta_2[/latex] and [latex]\beta_3[/latex] measure?

- What does economic theory predict about the signs of [latex]\beta_2[/latex] and [latex]\beta_3[/latex]?

- Use the data in the file “money.dat” to estimate the parameters of equation 8.37 using an OLS estimation procedure.

- At a 5% significance level, conduct appropriate hypothesis tests involving the coefficients [latex]\beta_{2}[/latex] and [latex]\beta _{3}[/latex] (i.e., test the predictions from part (b)).

- 17Scully (1974) investigated the effect of monopsony power on player salaries in major league baseball. Using a sample of 148 observations, Scully estimated the following equation as part of this study: \begin{equation*}\widehat{Log\text{\textit{(}Salary}_{i}\text{\textit{)}}}=\underset{(0.82)}{0.6699}+\underset{(4.76)}{1.0716}Log(\overline{\text{SA}}_{i})+\underset{(7.53)}{0.5220}Log(\text{M}_{i})\end{equation*}\begin{equation*}+\cdots +\underset{(3.10)}{0.2746}Log(\overline{\text{AB}}_{i})-\underset{(0.78)}{0.0621}Log(\text{SMSA}_{i})\end{equation*}

[latex]t[/latex]-statistics in parentheses

where:

- Salary[latex]_{i}[/latex] = 1968 or 1969 salary of player [latex]i[/latex] (non-pitchers)

- [latex]\overline{\text{SA}}_{i}[/latex] = lifetime slugging average of player [latex]i[/latex]

- M[latex]_{i}[/latex] = years in major league for player [latex]i[/latex]

- AB[latex]_{i}[/latex] = total lifetime at bats (# of years in majors} [latex]\times[/latex]5500)

- SMSA[latex]_{i}[/latex] = population in relevant standard metropolitan statistical area (SMSA)

(All variables are measured in log base 10.}

The [latex]\overline{\text{AB}}_{i}[/latex] variable requires a bit further comment. The numerator is the total number of times that a player is at bat. The denominator equals the average # of at bats for a major league player since, on average, a major league ballplayer bats 5500 times per season (Scully, p. 925). This variable will, in general, be larger for those players who play more innings and will be lower for players who spend a larger proportion of their time on the bench.

-

- What does each of the estimated slope coefficients measure? Interpret the economic meaning of each of the estimated parameters.

- How would the interpretation on the relevant coefficient change if the level of M[latex]_{i}[/latex] was used as a regressor instead of the log of M[latex]_{i}[/latex]?

- Which specification is more appropriate? (Hint: Think about whether earnings are expected to increase by a fixed absolute quantity or by a fixed percentage each year.)

- The file “fedbud.dat” contains data on total government recipts, total government outlays, spending on social security, and spending on national defense.

- Estimate the instantaneous rate of growth for each of the variables in this file.

- Use the equations estimated in (a) to generate predictions for each of these variables for the year 2024.

- Suppose that an econometrician estimates the following earnings equation:

\begin{equation*}\widehat{\text{earnings}_{i}}=16,000+700(\text{experience}_{i})-0.5(\text{experience}_{i}^{2})\end{equation*}

where: earnings[latex]_{i}[/latex] = earnings of person [latex]i[/latex] and experience[latex]_{i}[/latex] = years of work experience for person [latex]i[/latex].

-

- What is the marginal effect of a one-year increase in the level of work experience? Does this marginal effect vary with the level of work experience?

- Use a spreadsheet to create a graph illustrating the relationship between earnings and work experience

- Suppose that an econometrician estimates the following relationship between earnings and work experience for physicians (family practitioners only):\begin{equation*}\widehat{\ln (\text{earnings}_{i})}=11.23+0.12\text{experience}_{i}-0.00030\text{experience}_{i}^{2} \end{equation*} where: experience[latex]_i[/latex] = years of work experience for physician [latex]i[/latex].

- Use a spreadsheet program to construct a table illustrating the relationship between expected earnings and years of work experience for each of the first 20 years of work experience.

- Describe the relationship that appears to exist between the rate of growth in earnings and years of work experience under this estimated equation.

8.10 Mathematical Appendix

8.10.1 Returns to scale under the Cobb-Douglas production function

A production function is said to exhibit constant returns to scale if a proportionate increase in all inputs causes output to increase by the same proportion. Under a constant returns to scale production function, twice as much output is produced when twice as much of each input is used. A production function exhibits increasing returns to scale if a proportionate change in all inputs results in a proportionately larger change in output; decreasing returns to scale occur when output increases by a smaller proportion.

Defining [latex]\lambda[/latex] as scale factor measuring the change in input use ([latex]\lambda > 0[/latex]), and letting [latex]L_o[/latex] and [latex]K_o[/latex] represent the initial levels of labor and capital inputs, constant returns to scale are said to occur when:

[latex]f(\lambda L_o,\lambda K_o)=\lambda f(L_o,K_o) \tag{8.38}[/latex]

The expression on the left-hand side of equation 8.38 is the amount of output produced when inputs are scaled by a factor of [latex]\lambda[/latex]. If, for example, [latex]\lambda=2[/latex], this would be a measure of the amount of output produced when twice as much of each input are used. The right-hand side of equation 8.38 is equal to a change in output by a factor of [latex]\lambda[/latex]. If constant returns to scale hold, then output should change by the same proportion ([latex]= \lambda[/latex]) by which input use has changed.

Increasing returns to scale occur when:

[latex]f(\lambda L_o,\lambda K_o)>\lambda f(L_o,K_o) \tag{8.39}[/latex]

and decreasing returns to scale occur when:

[latex]f(\lambda L_o,\lambda K_o)<\lambda f(L_o,K_o) \tag{8.40}[/latex]

Since the Cobb-Douglas production function is defined as:

[latex]Q=\beta_oL^{\beta _1}K^{\beta _2}[/latex]

this production function will exhibit constant, increasing, or decreasing

returns to scale depending upon whether:

[latex]\beta_o(\lambda L_o) ^{\beta_1}(\lambda K_o)^{\beta_2}=\lambda (\beta_oL_o^{\beta_1}K_o^{\beta _2}) \tag{8.41}[/latex],

[latex]\beta_o(\lambda L_o) ^{\beta_1}(\lambda K_o)^{\beta_2}>\lambda (\beta_oL_o^{\beta _1}K_o^{\beta _2}) \tag{8.42}[/latex],

or:

[latex]\beta_o(\lambda L_o) ^{\beta_1}(\lambda K_o)^{\beta _2}<\lambda (\beta _oL_o^{\beta _1}K_o^{\beta _2}). \tag{c8.43}[/latex]

To determine whether the conditions under which the Cobb-Douglas production function exhibits constant, increasing, or decreasing returns to scale, note that the left-hand side of equations 8.41 -8.43 can be restated as:

[latex]\lambda ^{\beta_1+\beta_2}( \beta_oL_o^{\beta_1}K_o^{\beta_2})[/latex]

A comparison of this result with the right-hand side of equations 8.41 – 8.43 indicates that the Cobb-Douglas production function will exhibit constant, increasing, or decreasing returns to scale if:

[latex]\lambda ^{\beta_1+\beta _2}(\beta_oL_o^{\beta_1}K_o^{\beta_2}) =\lambda(\beta_oL_o^{\beta_1}K_o^{\beta_2}),\tag{8.44}[/latex]

[latex]\lambda ^{\beta_1+\beta_2}(\beta_oL_o^{\beta _1}K_o^{\beta_2}) >\lambda ( \beta_oL_o^{\beta_1}K_o^{\beta_2}), \tag{8.45}[/latex]

or:

[latex]\lambda ^{\beta_1+\beta_2}(\beta_oL_o^{\beta_1}K_o^{\beta_2}) <\lambda(\beta_oL_o^{\beta_1}K_o^{\beta _2}),\tag{8.46}[/latex]

respectively. An inspection of equations 8.44 -8.46 indicates that the Cobb-Douglas production function exhibits:

- constant returns to scale when [latex]\beta_{1}+\beta_{2}=1,[/latex]

- increasing returns to scale when [latex]\beta_{1}+\beta_{2}>1[/latex], and

- decreasing returns to scale when [latex]\beta_{1}+\beta_{2}<1[/latex].

8.10.2 Interpretation of the [latex]\beta _{j}[/latex] coefficients under the log-log specification}

In section 8.4.1, it was claimed that the estimated coefficients [latex]\beta_1,\beta _2,\ldots ,\beta_k[/latex] represent a measure of the percentage change in the dependent variable that results from a one-percent change in the level of the corresponding independent variable. This property can be easily demonstrated using calculus.

Proof:

Under the double-log specification, the population regression function may be written as:

[latex]\ln (Y)=\ln (\beta_{o})+\beta _{1}\ln (X_{1})+\beta_{2}\ln (X_{2})+\ldots+\beta_{k}\ln (X_{k})[/latex]

The total differential of this equation is:

[latex](\frac{1}{Y}) dY=\beta_{1}(\frac{1}{X_{1}})dX_{1}+\beta_{2}(\frac{1}{X_{2}}) dX_{2}+\ldots+\beta_{k}(\frac{1}{X_{k}}) dX_{k}[/latex]

If [latex]X_{j}[/latex] is the only parameter that changes, we can set [latex]dX_{s}=0[/latex] for[latex]s\neq j[/latex]. Thus, this equation becomes:

[latex]( \frac{1}{Y}) dY=\beta _{j}( \frac{1}{X_{j}}) dX_{j}[/latex]

Therefore:

[latex]\beta _{j}=\frac{\frac{dY}{Y}}{\frac{dX_{j}}{X_{j}}}[/latex]

This can also be stated as:

[latex]\beta_{j}=\frac{\frac{dY}{Y}\times 100\%}{\frac{dX_{j}}{X_{j}}\times 100\%}[/latex]

Expressed in this form, the numerator is a measure of the percentage change in [latex]Y[/latex] and the denominator is a measure of the percentage change in [latex]X_{j}[/latex].

[latex]\beta _{j}=\frac{\%\Delta \text{ in }Y}{\%\Delta \text{ in }X_{j}}[/latex]

8.10.3 Interpretation of the [latex]\beta_j[/latex] coefficients under the linear-log specification

In section 8.4.5, it was claimed that under a linear-log specification, the parameters [latex]\beta_1,\beta_2,\ldots ,\beta_k[/latex] equal:

[latex]\beta _j=\frac{\Delta Y}{\Delta X_j/X_j}[/latex]

Proof:

Under the linear-log specification, the relationship between the dependent and independent variables may be written as:

[latex][latex]Y=\ln (\beta_0)+\beta_1\ln (X_1)+\beta_2\ln (X_2)+\ldots +\beta_k\ln(X_k)[/latex][/latex]

The total differential of this equation is:

[latex]dY=\beta_1(\frac 1{X_1}) dX_1+\beta_2(\frac1{X_2}) dX_2+\ldots +\beta_k(\frac 1{X_k})dX_k[/latex]

If [latex]X_j[/latex] is the only parameter that changes, we can set [latex]dX_s=0[/latex] for [latex]s\neq j[/latex]. Thus, this equation becomes:

[latex]dY=\beta_j(\frac 1{X_j})dX_j[/latex]

Therefore:

[latex]\beta _j=\frac{dY}{dX_j/X_j}[/latex]

Replacing the differentials with differences, this becomes:

[latex]=\frac{\Delta Y}{\Delta X_j/X_j}[/latex]

8.10.4 Interpretation of the [latex]\beta _j[/latex] coefficients under the log-linear specification

In section 8.4.6, it was claimed that under a linear-log specification, the parameters [latex]\beta_1,\beta_2,\ldots ,\beta_k[/latex] equal:

[latex]\beta _j=\frac{\Delta Y/Y}{\Delta X_j}[/latex]

Proof:

Under the linear-log specification, the relationship between the dependentand independent variables may be written as:

[latex]\ln (Y)=\beta_o+\beta_1X_1+\beta_2X_2+\ldots +\beta_kX_k[/latex]

The total differential of this equation is:

[latex](\frac 1Y) dY=\beta_1dX_1+\beta_2dX_2+\ldots +\beta_kdX_k[/latex]

If [latex]X_j[/latex] is the only parameter that changes, we can set [latex]dX_s=0[/latex] for [latex]s\neq j[/latex]. Thus, this equation becomes:

[latex]( \frac 1Y) dY=\beta _jdX_j[/latex]

Therefore:

[latex]\beta _j=\frac{dY/Y}{dX_j}[/latex]

Replacing the differentials with differences, this becomes:

[latex]=\frac{\Delta Y/Y}{\Delta X_j}[/latex]

8.10.5 Marginal effects of a change in [latex]X_j[/latex] under alternative specifications

The marginal effect of a change in the level of an independent variable can be measured using basic calculus. If the dependent variable is a function of a single independent variable, the marginal effect of a change in the level of the independent variable is given by:

marginal effect of a change in [latex]X[/latex] = [latex]\frac{dY}{dX}[/latex]

A simple example of this appears in the case of the bivariate model:

[latex]Y=\beta_o+\beta_1X[/latex]

In this specification, the marginal effect of a change in [latex]X[/latex] is equal to:

[latex]\frac{dY}{dX}=\beta _1[/latex]

Since this effect is constant for all levels of [latex]X[/latex], we can note that this can also be expressed as:

[latex]\frac{\Delta Y}{\Delta X}=\beta _1[/latex]

Thus, as noted in Chapter 4, under the simple linear regression model, the marginal effect of a one-unit change in [latex]X[/latex] is equal to the slope parameter [latex]\beta _1[/latex].[9]

Reciprocal model

The reciprocal model is given by:

[latex]Y_i=\beta_o+\beta_1\frac 1{X_i}[/latex]

Under the reciprocal model, the marginal effect of a change in [latex]X[/latex] can be computed as:

[latex]\frac{dY}{dX}=\frac{-\beta_1}{X^2}[/latex]

Notice that under the reciprocal model, the marginal effect of a change in [latex]X[/latex] varies with the level of [latex]X[/latex]. In particular, the magnitude of the marginal effect becomes smaller as the level of [latex]X[/latex] increases.

Log-log models

A simple form of the log-log model is given by:

[latex]Y=\beta_oX^{\beta_1} \tag{8.47}[/latex]

or alternatively, as:

[latex]\ln (Y)=\ln (\beta_o)+\beta_1\ln (X) \tag{8.48}[/latex]

The marginal effect of a change in [latex]X_i[/latex] can be computed most easily by computing the differential of equation 8.48:

[latex]\frac 1YdY=\beta_1 \frac 1X)dX[/latex]

Thus, the marginal effect is given by:

[latex]\frac{dY}{dX}=\beta _1(\frac YX)[/latex]

Linear-log model

The linear-log model may be expressed as:

[latex]Y=\beta_o+\beta_1\ln (X) \tag{8.49}[/latex]

The differential of equation 8.49 is given by:

[latex]dY=\frac{\beta_1}XdX[/latex]

Thus, the marginal effect of a change in [latex]X[/latex] is given by:

[latex]\frac{dY}{dX}=\frac{\beta_1}X[/latex]

Log-linear model

The log-linear model may be expressed as:

[latex]\ln (Y)=\beta_o+\beta_1X \tag{8.50}[/latex]

The differential of equation 8.50 is given by:

[latex]\frac 1YdY=\beta _1dX[/latex]

Thus, the marginal effect of a change in [latex]X[/latex] is given by:

[latex]\frac{dY}{dX}=\beta_1Y[/latex]

Polynomial transformations

Linear model

The linear model is given by:

[latex]Y=\beta_o+\beta_1X[/latex]

As noted above, the marginal effect in this model is given by:

[latex]\frac{dY}{dX}=\beta_1[/latex]

Quadratic model

The quadratic model can be expressed as:

[latex]Y=\beta_o+\beta_1X+\beta_2X^2[/latex]

Under this model, the marginal effect of a change in [latex]X[/latex] is given by:

[latex]\frac{dY}{dX}=\beta_1+2\beta_2X[/latex]

Cubic model

The cubic model can be expressed as:

[latex]Y=\beta_o+\beta _1X+\beta_2X^2+\beta_3X^3[/latex]

Under this model, the marginal effect of a change in [latex]X[/latex] is given by:

[latex]\frac{dY}{dX}=\beta_1+2\beta_2X+3\beta_3X^2[/latex]

8.10.6 Elasticities under alternative specifications

Elasticity is a measure of the percentage change in a dependent variable resulting from a one-percent change in the level of an independent variable.

The elasticity of [latex]Y[/latex] with respect to [latex]X[/latex] is given by:

[latex]E_{YX}=\frac{\text{\% }\Delta \text{ in }Y}{\text{\%}\Delta \text{ in }X}[/latex]

[latex]=\frac{\frac{\Delta Y}Y\times \text{ 100\%}}{\frac{\Delta X}X\times \text{100\%}}[/latex]

[latex]=\frac{\frac{\Delta Y}{\Delta X}}{\frac YX}[/latex]

For nonlinear relationships, the elasticity of [latex]Y[/latex] with respect to [latex]X[/latex] is measured as:

[latex]E_{YX}=\frac{\frac{dY}{dX}}{\frac YX} \tag{8.51}[/latex]

The numerator in equation 8.51 is the slope of a tangent line to the function. This numerator is the marginal effect discussed in the preceding section. The denominator in equation 8.51 is the ratio of [latex]Y[/latex]to [latex]X[/latex]. As equation 8.51 indicates, elasticity may vary as the level of [latex]X[/latex] changes (due to changes in either the slope or the ratio of [latex]Y[/latex] to [latex]X[/latex]).

Using the results from the previous section, elasticity can be easily computed for each of the functional forms discussed in this chapter. Table 8.1 in the main body of this chapter contains a listing of the elasticity measures corresponding to each functional form.

- More precisely, when the dependent variable ([latex]Y[/latex]) is a function of a single independent variable ([latex]X[/latex]), the marginal effect is measured by the derivative ([latex]\frac{dY}{dX}[/latex]). If the dependent variable ([latex]Y[/latex]) is a function of a set of k independent variables [latex](X_{1},\ldots ,X_{k})[/latex], then the marginal effect of a change in the [latex]j[/latex]th independent variable is measured by the partial derivative ([latex]\frac{\partial Y}{\partial X_{j}}[/latex]). ↵

- In the special case of a bivariate relationship, an examination of a scatterplot of the dependent and independent variables will often suggest an appropriate specification. Scatterplots, however, are not very useful for this purpose in a multiple regression framework. Even in the case of bivariate regression relationships, though, model specifications based on observed data, rather than on an appropriate model of the underlying causal relationships, may lead to results that are misleading, and nongeneralizable to other samples. ↵

- The theoretical basis of age-earnings profiles is discussed in Becker (1993). Most current studies of the empirical relationship between age and earnings are based on the seminal work of Mincer (1974). ↵

- All members of this particular sample are full-time workers. The work experience variable is defined as the total number of months spent working at the worker's two most-recent jobs (including the present job). Most studies, however, use a different measure of work experience that is based upon the number of years worked. In particular, many econometricians have followed Mincer (1974) in defining work experience as age minus years of schooling. The data used to generate the results reported below is a subsample drawn from the National Longitudinal Study of the High School Class of 1972. In this data set, the only measure of recent work experience is a series of questions that ask the respondent for the starting and ending dates for their most recent jobs. This information has been used to generate the measure of recent work experience used in this equation. The data used in this estimation can be found in the file ``exp1.dat.'' ↵

- One of the reasons for the difference in the magnitude of the coefficients in this equation is the rather large difference in the magnitude of these variables. In the early years of computing, it was often necessary to rescale variables so that they were all measured in units of comparable magnitude. (The effects of rescaling variables is discussed in Chapter 9.) The reason for this was the possibility of substantial rounding error when units of substantially different magnitude were used in a regression. Most modern regression packages, however, are not affected by differences in the magnitude of different variables. While OLS regression estimates are not generally affected by rounding error caused by differences in the magnitude of different variables, differences in the scale of variables still presents a problem for some of the iterative estimators discussed in later chapters of this text. ↵

- As the level of work experience increases, the variable ``experience[latex]^{2}[/latex]'' increases more rapidly than the variable ``experience.'' Thus, at low levels of experience, the effect of the positive coefficient on ``experience'' dominates the negative effect of the ``experience[latex]^{2}[/latex]'' term. Since ``experience[latex]^{2}[/latex]'' increases more rapidly than ``experience,'' log-earnings rise by progressively smaller amounts (and will eventually decrease) as the level of work experience rises. ↵

- Proof: The basic form for this earnings equation is given by: \begin{equation*} \ln (Y_{i})=\beta _{o}+\beta _{1}X_{i}+\beta _{2}X_{i}^{2} \end{equation*} where [latex]Y_{i}[/latex] equals earnings of person [latex]i[/latex] and [latex]X_{i}[/latex] equals months of work experience for person [latex]i[/latex]. The total differential of this equation is given by: \begin{equation*} \frac{1}{Y_{i}}dY_{i}=\left( \beta _{1}+2\beta _{2}X_{i}\right) dX_{i} \end{equation*} For small changes in [latex]X_{i}[/latex], this relationship can be restated as: \begin{equation*} \frac{\Delta Y_{i}}{Y_{i}}\approx ( \beta _{1}+2\beta _{2}X_{i})\Delta X_{i} \end{equation*} or: \begin{equation*} \frac{\Delta Y_{i}}{Y_{i}}\times 100\%\approx ( \beta _{1}+2\beta_{2}X_{i}) \Delta X_{i} \times 100\% \end{equation*} This simplifies to: \begin{equation*} \%\Delta \text{ in }Y_{i}=\left( \beta _{1}+2\beta _{2}X_{i}\right) \DeltaX_{i}\times 100\% \end{equation*} ↵

- It should also be noted that the experience variable used here is not a very accurate measure of actual work experience since it only measures the total number of months worked at the two most recent jobs (including the current job). ↵

- More generally, the dependent variable is assumed to be a function of more than one independent variable. In this case, the marginal effect of a change in a single independent variable is captured by the partial derivative:

marginal effect of a change i[latex]n X_j = \frac{\partial Y}{\partial X_j}[/latex]

In the multiple regression equation given by:[latex]Y_i=\beta _o+\beta _1X_{1i}+\beta _2X_{2i}+\cdots +\beta _kX_{ki}+u_i[/latex]

the marginal effect of a change in a particular independent variable, [latex]X_{ji}[/latex], is given by:[latex]\frac{\partial Y}{\partial X_j}=\beta _j[/latex]

↵